READ OUR PUBLICATIONS

We send monthly newsletters to our clients, colleagues, and interested parties.

From Our Family to Yours: 4 Ways to Teach Kids About Money

Teaching kids about money in the Digital Age isn’t always easy. Between online shopping, direct-deposit paychecks and banking by app, today’s children are growing up in a world where they may rarely experience a cash purchase or even a monetary transaction. To kids, it can look like the next item...

Berkshire Trip 2018

In early May, I attended the Berkshire Hathaway shareholder meeting in Omaha, Nebraska. The event, dubbed “Woodstock for Capitalists,” attracted more than 40,000 attendees from around the world.

All-Weather Portfolio Construction

It seems that there has been an increase in severe weather these days including floods, fire, and wind. In Savannah, we suffered a direct hit from Hurricane Matthew last year and endured a mandatory evacuation this year due to Hurricane Irma. Hurricanes are a constant threat during the summer and...

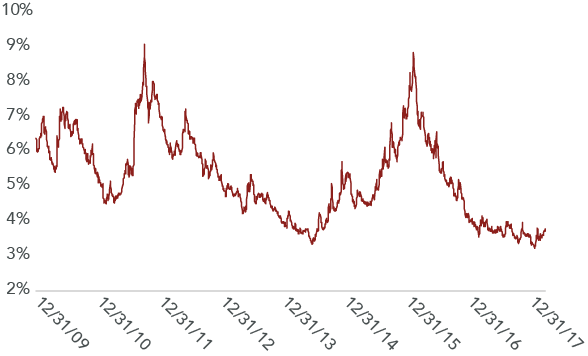

Notes from the Investment Team

2017 was another banner year for investors. The total return (inclusive of dividends) for the S&P 500 was a gain of 22%. There were not any meaningful hiccups along the way; as shown in the chart below, the index posted positive returns in every single month of 2017. International stocks fared even...

An Antidote to Volatility

“Antidote”: Something that works against an unwanted condition to make it better.

Keeping Our Eyes on Access to Capital

In 2007, you could count the number of companies with a “AAA” credit rating on two hands. General Electric (GE) was among that select group. But decisions made by management over the preceding 10-15 years eventually led GE to lose that top credit rating in 2009 – and seriously tested the company’s...

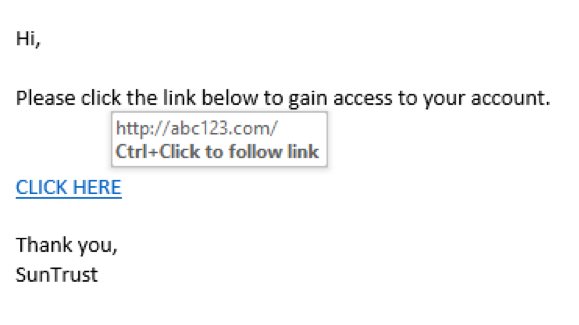

Indentity Theft

Most people have been, or know someone who has been, affected by identity theft. It happens to those in their 20’s, those in their 90’s, and to all ages in between. According to the Federal Trade Commission, identity theft occurs when someone uses personally identifying information (PII) without...

Notes from the Investment Team

2017 was another banner year for investors. The total return (inclusive of dividends) for the S&P 500 was a gain of 22%. There were not any meaningful hiccups along the way; as shown in the chart below, the index posted positive returns in every single month of 2017. International stocks fared even...

Estate Planning For Life!

Estate planning is really “transfer planning.” It is an ongoing exercise of planning how you accumulate, conserve, and distribute your assets during life, at death, and beyond. There are both financial and non-financial reasons to plan. These range from minimizing income and estate taxes,...

Investment Approach Revisited

The S&P 500 continued its march higher in the third quarter and has now increased by 14% (including dividends) in 2017. International markets have reported even better results, with the MSCI World index (ex-U.S.) climbing 21% over the same period.