The S&P 500 continued its march higher in the third quarter and has now increased by 14% (including dividends) in 2017. International markets have reported even better results, with the MSCI World index (ex-U.S.) climbing 21% over the same period.

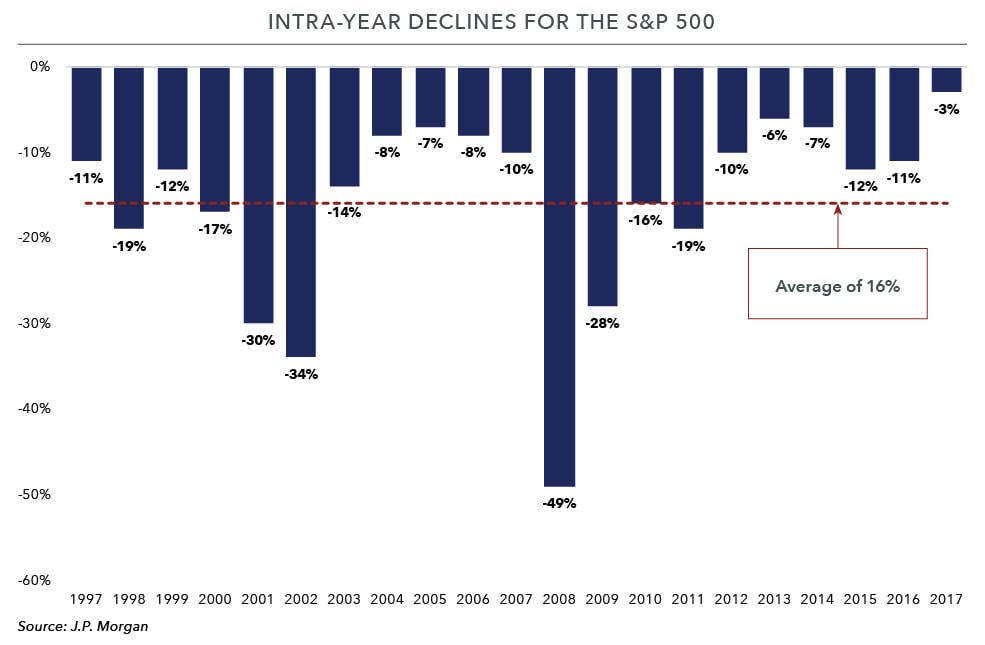

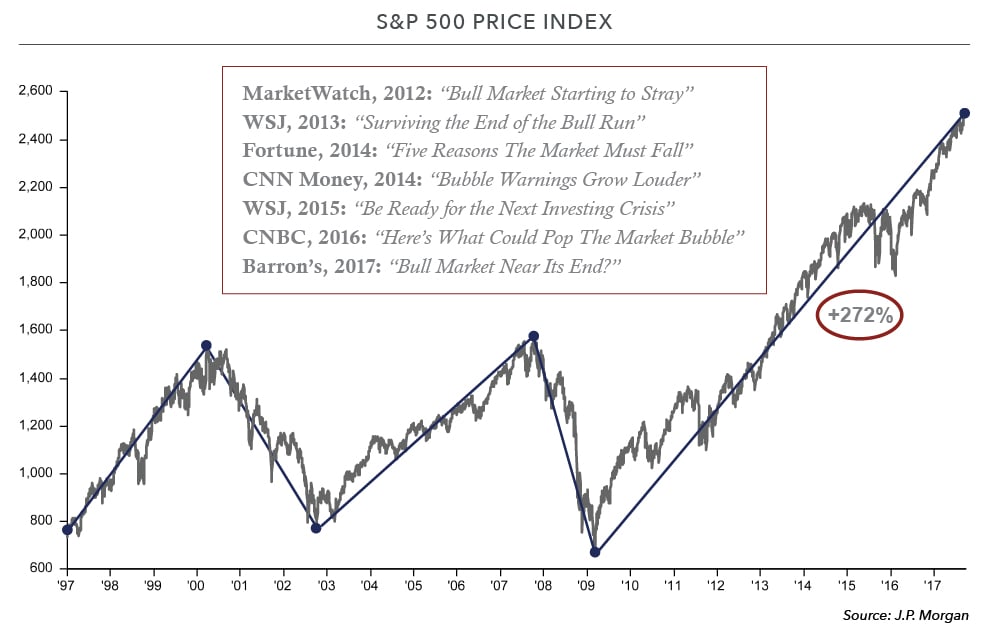

This marks the continuation of eight bountiful years for investors since the end of the financial crisis. From the March 2009 lows, the S&P 500 has risen from 676 to 2,519 – a cumulative increase of roughly 270%, before dividends. In addition, the environment has been unusually tranquil, particularly in the past few quarters. Since the U.S. presidential election, the largest drawdown for the S&P 500 has been less than 3%. To put that in context, the average intra-year decline for the index over the past two decades has been in the double digits.

Life is good when you can get outsized returns and low volatility. Inevitably, this too shall pass as markets don’t move in a straight line. There will be periods of heightened volatility and falling stock prices (and they will probably coincide). Significant, unpredictable corrections are an unavoidable part of investing in stocks.

While the intrinsic value of the index (or more accurately, of the businesses in the index) steadily increases over time, the valuation (price) attributed to these businesses is subject to the whims of market participants. Historically, changes in market prices have been significantly larger than what is justified by changes in underlying business results. Said differently, investor psychology is what drives short-term changes in stock prices, not business fundamentals.

As Philip Carret, manager of one of the first mutual funds, said nearly a century ago, “Stock market trends reflect the buying and selling of thousands of human beings… At one time their hopes and at another their fears affect prices more vitally than steel production, carloadings, or any other business fact.”

Predicting the timing and magnitude of shifts in investor sentiment is difficult to do; successfully doing it with any consistency is nearly impossible. It is not the basis of a sound long-term investment strategy. Consider the short list (in the chart below) of negative headlines from leading financial publications over the past few years. These articles are a dime a dozen – and new ones are written all of the time. When some market prognosticator is eventually proven right (due to nothing more than fortuitous timing), remember that he has likely been predicting a similar outcome for a long time – and and has almost certainly missed most of the equity market gains achieved over the past eight years.

Where the stock market will go next week or next year is anybody’s guess. We operate under the belief that investors will continue to move between euphoria and despair, just as they’ve done in the past. In either environment the tenets of our approach are constant. In this newsletter, we thought it would be helpful to reiterate our investment philosophy to ensure clients understand the way we think about managing their capital.

Risk Management

Individual client circumstances inform our investment decisions. Those circumstances directly influence the asset allocation in client portfolios (the balance between stocks and bonds). Our goal is to intelligently balance these asset classes to adequately capture the benefits they provide for investors while also remaining cognizant of their shortcomings.

We think about risk in two ways: capacity and willingness to bear risk.

Capacity to bear risk is based on quantitative factors such as your age, financial resources, and future cash needs. Willingness to bear risk, on the other hand, is qualitative in nature, unique for each person, and subject to change. It may be different for two individuals who are the same age with identical financial circumstances.

Industry data has shown that the long-term performance of the average investor has trailed the returns of the market indices by a wide margin. A recent study by Blackrock estimates that the average investor earned 2.3% per year in their portfolio over the two decades from 1997 – 2016, compared to a 7.7% annual return for stocks and a 5.3% annual return for bonds over the same period. This discrepancy reflects the inability of the average investor to stay committed to a long-term investment strategy during periods of heightened volatility like the financial crisis of 2007 – 2009.

An accurate assessment of risk tolerance is a prerequisite for intelligent portfolio construction. Our objective is to set asset allocations so clients will have the conviction to stay invested throughout the market cycle.

Independent Research

We make investment decisions based on in-depth due diligence using various resources, including corporate filings, third-party research, industry contacts and proprietary models.

Our objective is to find high-quality companies with sustainable competitive advantages. Those advantages are what enable companies to generate excess returns and produce better than average results for the owners of the business.

In many cases, our ability to find attractive investments is less about information arbitrage (knowing something truly unique) than it is about time arbitrage. Because we’re willing to think and invest with a long-term view, how we think about companies (and as a corollary, the opportunity set we’re attracted to) differs from many market participants and Wall Street analysts.

For our clients, this is key to understanding how we think about investing: short-term volatility, combined with a fair amount of patience, is what gives us the opportunity on occasion to buy high-quality companies at a discount to fair value. Without the wide swings in securities prices that (understandably) create much angst for clients, we wouldn’t be able to find new investment opportunities.

Diversification

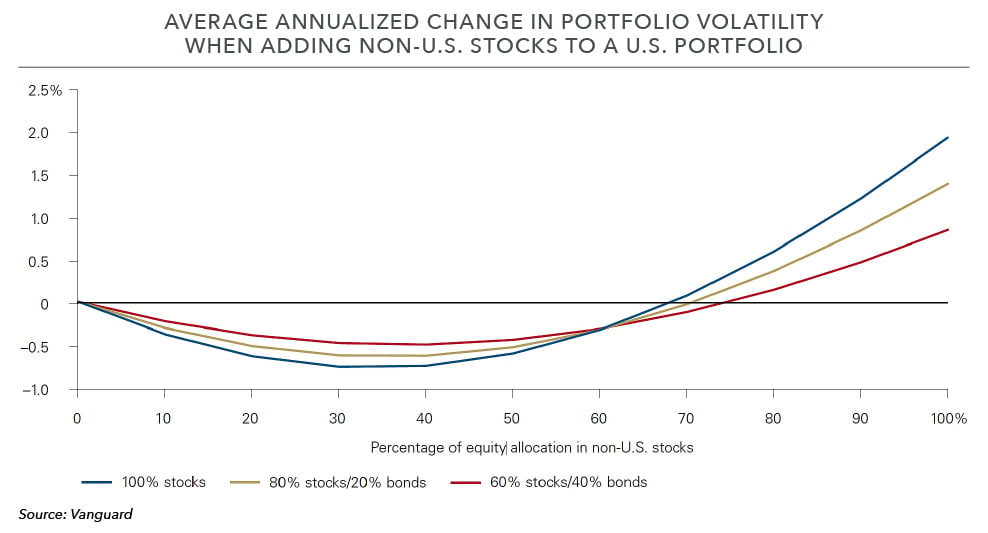

We believe clients are best served by holding globally diversified portfolios. Historically, diversification across non-correlated asset classes and geographies has resulted in reduced portfolio volatility and (as a result) better risk-adjusted returns. This is as close as you get to a “free lunch” in investing. As shown below, allocating 20% – 40% of your equity portfolio to international stocks has historically resulted in lower portfolio volatility (relative to a 100% allocation to the S&P 500) at comparable rates of return.

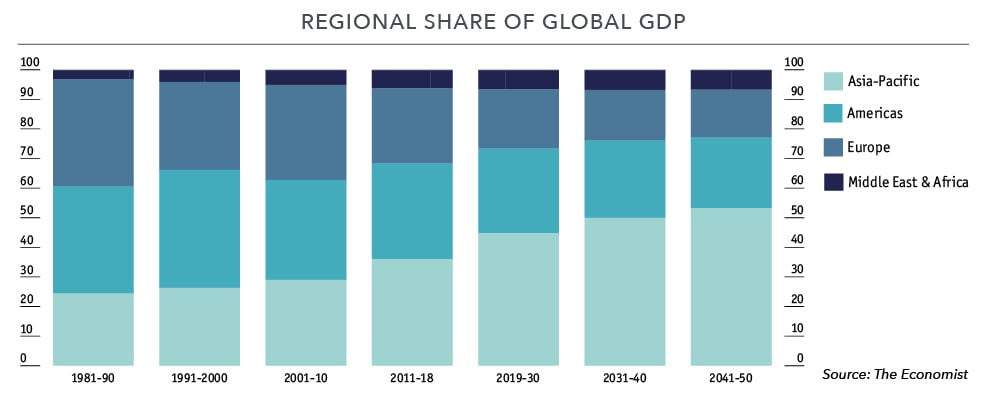

In addition to reduced portfolio volatility, we believe there’s a strong argument to be made for individuals living in the United States to expand their investment purview beyond their home country. It’s worth noting that non-U.S. markets account for 50% of the global market cap of publicly-traded companies, 80% of global GDP, and 95% of the world’s population. As shown below, the share of global GDP attributable to countries outside the U.S. is increasing as well (this reflects outsized population and productivity growth).

The benefits of diversification are only attainable if there’s a long-term commitment to the asset allocation. We build portfolios with the appreciation that certain regions and certain asset classes will have their day in the sun. When you review your account statement and see one asset class outperforming another, remember that these components should not be analyzed in isolation – they each have a role to play in a portfolio.

Market Cycles

We believe there’s value in trying to “take the pulse” of the market and the broader economy. We want to understand the current state of affairs so we have a sense for whether investors and consumers are optimistic, pessimistic, or somewhere in between. We’re not trying to predict where the world is heading; we’re trying to get an idea of where we are. To the extent we see outliers in either direction, that influences our investment outlook.

We track several indicators, including the health of credit markets and the valuation of equity markets relative to historic averages. As sentiment shifts through the market cycle, our objective is to maintain a thoughtful and consistent investment approach. As the crowd swings between bouts of euphoria and despair, we endeavor to stay closer to the middle of the spectrum.

Long-Term Focus

As discussed above, we have a long-term time horizon. As a corollary, we also have a low turnover bias. While asset allocation and security selection drive the investment process, we’re mindful of the costs and tax implications associated with portfolio management decisions.

The U.S. tax code incentivizes long-term equity ownership. We’ll spare you from the calculations, but consider one example: assuming a 20% long-term capital gains rate, an investor that invests $1 million in a single stock for ten years with 10% pre-tax (annualized) returns will end up with $2.28 million (an after-tax return of 8.6% per year).

By comparison, if the investor sold and then purchased a new stock at the end of each year and still achieved 10% pre-tax returns, she would end up with $2.16 million (an after-tax return of 8.0% per year).

The buy-and-hold investor ends up ahead by $120,000. This is due to the value created by deferring the tax liability. Over time, the cost of sending a check to Uncle Sam is compounded, with the gap between the two scenarios growing wider (the math is even more compelling when you consider short-term capital gains can be at rates considerably higher than 20%). Over the course of decades, a point or two a year of excess returns makes a real difference.

Conclusion

By staying focused on client goals, employing prudent diversification, and performing thorough due diligence on our investments, we endeavor to position clients for long-term success.