In 2007, you could count the number of companies with a “AAA” credit rating on two hands. General Electric (GE) was among that select group. But decisions made by management over the preceding 10-15 years eventually led GE to lose that top credit rating in 2009 – and seriously tested the company’s financial stability. Consider, for example, the growth of the company’s finance division, GE Capital, which was created in the early 1930’s to facilitate customer purchases in the industrial business. Over time, the focus of GE Capital shifted from industrial purchases into the financing of other assets, including subprime mortgages, auto loans, and credit-card debt. GE capitalized on its “AAA” credit rating, raising billions and billions of dollars of low cost debt. By 2007, GE Capital was big enough to qualify as one of the largest banks in the country and accounted for the majority of GE’s profits.

In addition to expanding its scope, GE Capital made the fateful decision to finance roughly $100 billion of its balance sheet through short-term borrowings (commercial paper). They did that because long-term debt meant higher interest expense and lower quarterly earnings. As opposed to bonds with a 4% or 5% coupon, why not just borrow short-term funds at a lower cost?

What they accepted with that decision (knowingly or otherwise) was financing risk. That was a nonissue until it wasn’t: when the credit markets spigot turned off in 2008, GE Capital struggled to rollover the commercial paper needed to fund its business. The duration mismatch between the assets and liabilities on its balance sheet nearly brought General Electric to its knees. The stock price, from a high of $42 per share in September 2007, was down nearly 85% by early 2009.

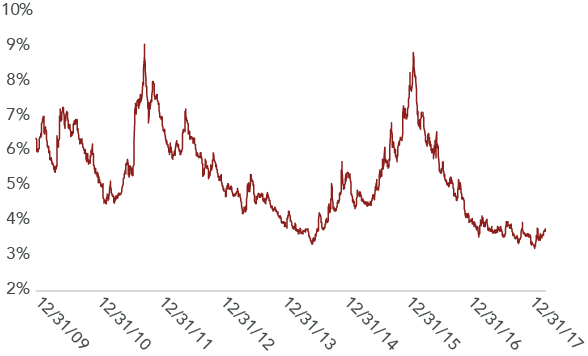

A lot has changed in the decade since 2008. Access to capital is only a concern for the most speculative borrowers. In addition to historically low nominal interest rates and a flat yield curve, high-yield spreads, as shown below, have tightened in recent years (high-yield spreads measure the extra cost paid by non-investment grade companies to issue debt). As a result, borrowers have been able to inexpensively issue or refinance debt, regardless of their financial situation.

U.S. High Yield Spreads

The same trend can be seen in equity markets, where higher stock prices and a willingness to suspend disbelief has allowed businesses in need of outside capital to cost-effectively raise funds from the investing public. As an example, meal delivery kit company Blue Apron (APRN) went through an IPO in July 2017, raising $300 million. Considering that cash outflows to fund the business exceeded $200 million (cumulatively) over the preceding three years, including $150 million in 2017 alone, access to capital was critical.

But then market participants became skeptical. Currently, with the stock down roughly 80% from its IPO price of $10 per share, the company’s options are greatly restricted. Going back for another large equity raise would be enormously dilutive. To avoid that outcome, the company has significantly cut back on operating expenses, including a more than 30% reduction in advertising expenses in the fourth quarter of 2017. The problem is that marketing drove customer trials and sales growth for Blue Apron. As a result, the company reported a 15% decline in customers in the fourth quarter. The flywheel is now spinning in the wrong direction. Without access to outside capital at reasonable terms, Blue Apron’s business model is under threat.

We think automobile manufacturer Tesla (TSLA) is another example worth reviewing. The company has relied on capital markets for billions of dollars to support ongoing research and development and to the supply the capital necessary to ramp vehicle production. As a result, Tesla has more than $10 billion of debt on its balance sheet. They’ve also tapped equity markets, with the number of outstanding shares increasing 55% over the past five years. If investors continue to believe in the company and management (primarily CEO Elon Musk), Tesla should be able to cost-effectively fund its future investments. On the other hand, if market participants become skeptical or risk averse, Tesla would be forced to make some tough decisions.

We recently heard a Tesla bull argue, after admitting that the company has an unhealthy balance sheet, that capital markets are the answer: “There are plenty of people who will give Elon money at almost no cost.” He viewed that as a positive (and there’s no question that’s a great spot to be in if you’re the one raising capital). The question we ask ourselves as investors is whether those conditions can change (they can) – and if they do, what impact would that have on the business?

In both cases, we think there’s a risk outside of management’s direct control that is difficult (or impossible) to handicap. That’s not the type of risk we’re comfortable assuming for clients.

Just to be clear, there’s nothing wrong with tapping capital markets. But you’re in a dangerous situation if it’s a prerequisite to support your business. While the timing is unknown, there will be periods in the future where capital markets will be less accommodating than they are today.

Howard Marks, the co-founder of Oaktree Capital, explains why it can be a real problem if your business model or financing is dependent upon permanent access to outside capital:

“To succeed you have to survive. It’s not enough to survive ‘on average’; you have to survive on the worst days. Never forget the six-foot tall man who drowned crossing the stream that was five feet deep on average.”

On the other end of the spectrum are companies that accept short-term costs in exchange for long-term predictability (as an example, relying on more expensive long-term debt as opposed to commercial paper). This mindset doesn’t just apply to financing the business. It also includes the willingness to bear short-term pain (lower earnings in the near term) to support future earnings growth and to improve the long-term competitive position of the business. Their managers are willing to make the necessary investments to support long-term value creation. Historic results suggest you will do well over an investment lifetime if you own businesses with managers that take this approach.

Conclusion

At the depths of the financial crisis in October 2008, General Electric secured $3 billion of financing from Berkshire Hathaway with terms they would have scoffed at as ridiculously expensive months earlier (preferred stock with a 10% dividend, as well as warrants that gave Berkshire the option to buy GE shares over the next five years at a fixed price). In addition, GE raised another $12 billion of capital through public equity markets (at prices that were well below where the stock traded a year earlier). Their reliance on commercial paper, which helped boost earnings per share in the short-term, ultimately came at a significant cost to shareholders.

It’s worth noting that GE raised these funds on short notice – and just six days after GE CEO Jeff Immelt told investors that “we feel very secure about how the funding looks.” He was wrong. As later reported in Fortune, “GE needed a sudden, huge, and utterly unexpected emergency infusion of cash.” That goes to show you just how quickly things can change when a real panic breaks out.

When Warren Buffett published his annual letter to shareholders in early 2009, here’s what he said about the GE deal (and similar deals he agreed to during the depths of the crisis in 2008):

“We never want to count on the kindness of strangers in order to meet tomorrow’s obligations. When forced to choose, I will not trade even a night’s sleep for the chance of extra profits.”

Thankfully, with common sense and a long-term perspective, we think investors can have their cake and eat it too. As Buffett has shown over his fifty-plus years at Berkshire Hathaway, you can sleep tight and make plenty of money investing in financially sound, high-quality businesses.

It’s worth noting that Berkshire was only in the position to secure that deal with GE in October 2008 because they held ample liquidity on their balance sheet in the years prior to the financial crisis (north of $50 billion in cash and equivalents). Berkshire was able to act aggressively and capitalize on opportunities at the bottom because they avoided the worst excesses near the top.

Market volatility has picked up in early 2018. Time will tell if we’re entering a more discriminating capital markets environment. If that’s the case, businesses that rely upon unbounded access to outside capital are susceptible to changes in investor risk tolerances. If we’ve done our job properly, the companies held in your portfolio will not need to rely on the kindness of strangers to make ends meet.