The technology industry has gained significant stock market influence since the widespread use of the internet in the mid-to-late 1990s. Many investors recall the initial "dot-com bubble" of the late 1990s, the highly speculative exuberance that followed from investors chasing fads, and the subsequent bear market when the bubble finally burst in 2001.

More than 20 years later, technology companies have matured and are now among the world's most dominant and established corporations, outgrowing traditional blue chip stocks and impacting the overall market on several levels. It's important to understand how the technology industry concentration affects today's market, often gauged by the S&P 500, a key stock market index that measures the performance of 500 large-cap U.S. companies listed on major stock exchanges.

Changes to the S&P 500

Established in 1957, the S&P 500 can provide a snapshot of the overall health and direction of the U.S. economy. The S&P 500 is a market cap-weighted index; in other words, an index where each stock's weight is determined by its market value. Therefore, the influence of the companies on the index will shift as they grow at different rates over time.

In the previous decade, tech companies have dramatically increased their market caps, reflecting the growing impact that technology has played in our lives over the last 20 years. Reasons for this surge include the tech industry's focus on relentless innovation, a global audience, and the disruption of traditional industries. Companies like Apple, Amazon, Microsoft, Meta, and Alphabet have revolutionized e-commerce, cloud computing, digital entertainment, and the emerging artificial intelligence industry.

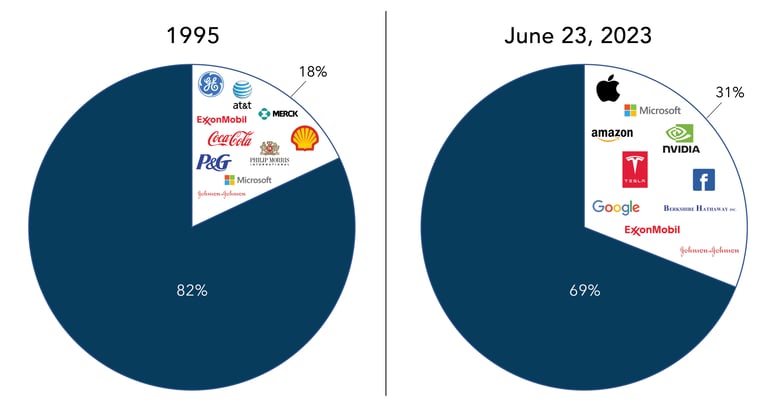

In 1995, the top 10 S&P 500 companies represented just 18% of the S&P 500 (GE, AT&T, Exxon, Coke, Merck, Royal Dutch, Philip Morris, Procter & Gamble, Johnson & Johnson, and Microsoft), but as of June 23, 2023, the top 10 index components represented 31% (Apple, Microsoft, Amazon, Nvidia, Tesla, Google, Facebook, Berkshire Hathaway, Exxon, and Johnson & Johnson).

Along with the reshuffling of global brand names in the S&P 500, a dramatic change is the concentrated industry weighting now seen in the index. The S&P 500 has always been a cap-weighted index, but historically the top index constituents have been better diversified across economic sectors. With the S&P 500 becoming top-heavy, technology companies considerably influence the index's overall performance. The diversification benefits of using the S&P 500 have arguably declined, leaving investors making more concentrated investments than they may realize.

The top five stocks in the S&P 500 currently account for 24% of the value, and Apple and Microsoft represent more than 14% combined. The Russell 2000 is a market cap-weighted index commonly used to track small-cap stocks. Apple is now larger than this entire index.

A newcomer to the top of the S&P 500 is graphics card maker Nvidia. This company's meteoric growth has made them the fourth largest member of the S&P 500 in a relatively short period. At the end of 2014, the company ranked 337th in the index. Based on Nvidia's expansion into artificial intelligence, growth will likely continue. However, it is yet to be determined if Nvidia's stock will outperform going forward. It very well may, but expectations are high, and the company's stock price has demanded a significant premium.

Owning exposure to success stories like Nvidia is a feature of index investing. However, we caution against holding too much of any one stock. Nvidia joined the S&P 500 in November 2001, taking the spot previously occupied by Enron. We draw no similarities between the two companies and greatly admire what Nvidia has built. Still, the world changes fast, and as fiduciaries, we seek to protect against the worst outcomes. Enron had become the seventh largest company in the index before its downfall. Change is constant, and companies will continue to gain or lose status in the S&P 500.

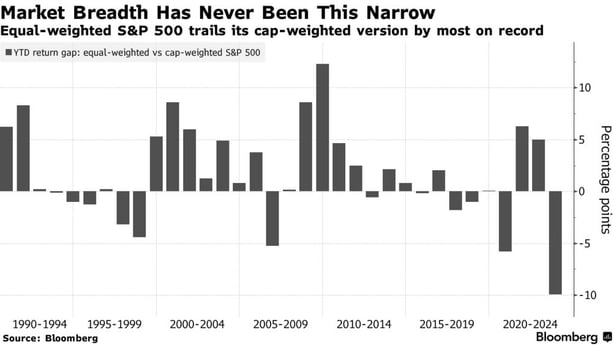

A Narrow Market

2023 has been a historically narrow market with seven mega-cap stocks (Apple, Microsoft, Amazon, Nvidia, Alphabet, Tesla, and Meta), leading the S&P 14.1% higher and contributing 83% of the total year-to-date return. As of June 23, 2023, the average return of the top 7 stocks is 87%, while the average return from the rest of the S&P 500 is just 3%.

These mega-cap growth stocks weighed the market down in 2022. Apple stock was down 27% year-over-year, but still better than fellow tech giants Amazon (down 51%), Meta (down 70%), and Alphabet (down 34%). Ultimately, the S&P 500 overall was down 18% and was effectively "pulled downward" by tech company performance. Because so few stocks at the top — with similar characteristics — significantly impact the overall index, volatility at the top amplifies index performance.

As seen below, over the past 20 years, using an equal-weighted S&P 500 index (EWI) would have added value relative to the market cap-weighted index.

%20-%20Cumulative%20total%20return%20(Jan.%202003%E2%80%93Dec.%202022).png?width=745&height=258&name=S%26P%20500%C2%AE%20Equal%20Weight%20Index%20(EWI)%20-%20Cumulative%20total%20return%20(Jan.%202003%E2%80%93Dec.%202022).png)

Risk Management Through Portfolio Construction

The S&P 500 is a basket of companies correlated with the health of the U.S. economy; however, the indices' market-cap weighted composition may represent a skewed view of what's happening in the broader stock market. When investing in a product that tracks the S&P, you have a relatively concentrated portfolio. Many top holdings are excellent companies, but the question is whether they represent attractive investments at today's prices.

One risk management strategy to protect assets is position sizing. Avoiding a single stock becoming too large diminishes the chances of one company having an outsized adverse effect on the portfolio. The Fiduciary Group investment team intentionally structures stock holdings to avoid overexposure to any industry or end market.

If history is any indication, the top performers of the next decade are likely to be different from the last. We will continue to seek out businesses performing well at attractive valuations. Those companies typically have solid balance sheets, competitive advantages, and capable management teams.

There is a natural emphasis on stock selection when discussing investments; however, stocks are only one component of designing an asset allocation. As fiduciaries, we focus on building a mix of assets that will preserve capital and grow assets in the future. Diversifying across asset classes and geographies consistent with the client's objectives, risk tolerance, and time horizon is at the forefront of portfolio construction.

Please feel free to contact us if you have questions or would like to discuss your investment strategy.