In response to 11 Fed interest rate increases since March 2022, savers should reconsider the wisdom of “parking” cash in a traditional bank savings account and explore investment options that carry relatively low risk in today’s higher interest environment. The rise in interest rates offers opportunities for investors who want to earn returns that complement their existing portfolio but are not directly tied to market swings or market volatility.

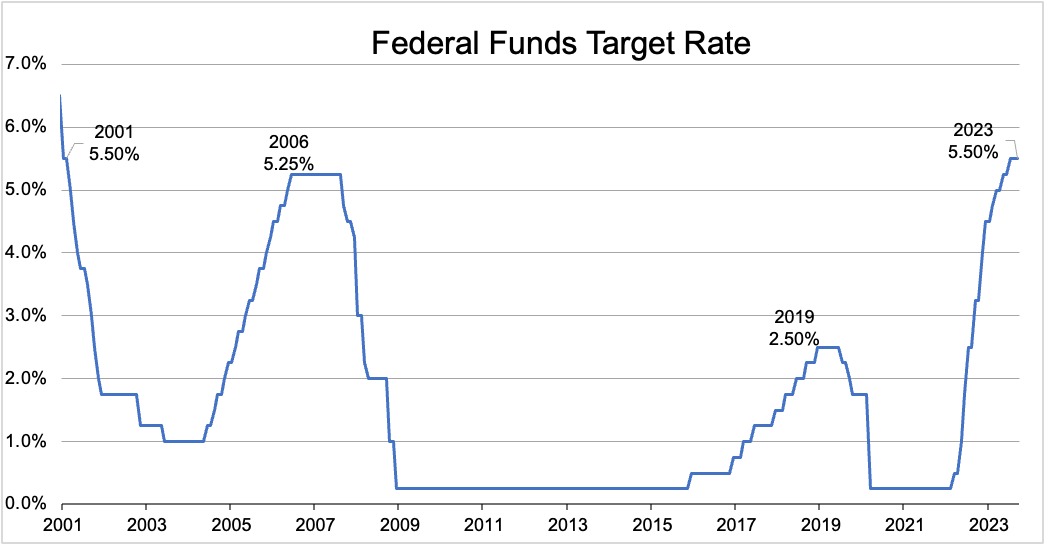

Interest rate hikes and tightening monetary policy in general are implemented by the Federal Reserve to ease inflation, which peaked at 9.1% in June 2022. This strategy seems to be working, as the U.S. inflation rate has decelerated to 3.7% as of September 2023, leaving many to wonder if the Fed is finished hiking. While they will not say for sure, the Fed has held rates constant during their last two meetings, which occurred on September 20th and November 1st. If you look at the futures market, it is betting that the Fed will not have to raise again, and the futures market is implying a 45% probability that the Fed will cut rates by the summer of 2024. That said, nobody knows what the future holds for rates.

Futures Market - Fed Action Probability

| Fed Meeting Date | Probability of Rate +Hike / -Cut |

| 12/13/2023 | 27.1% |

| 3/20/2024 | -14.5% |

| 6/12/2024 | -44.7% |

| 9/18/2024 | -58.0% |

| 12/18/2024 | -49.9% |

Source: Bloomberg

Notwithstanding what the Fed may decide in the future, interest rates are now higher than they’ve been since early 2001, offering opportunities for conservative investors. Whether it’s excess that has built up in your checking or savings that you have yet to put to work, cash from selling assets, or even emergency fund cash, you owe it to yourself to ensure it is earning a competitive interest rate. To take advantage of higher interest rates, consider exploring low-risk opportunities to “hold” excess cash – from money market accounts to various low-risk bond types.

Low-Risk Options

In today’s higher-interest economic environment, several low-risk options might make sense for investors who want their cash to earn stronger returns than a traditional savings account.

Five low-risk options we typically consider for our clients include:

1. Money Market

A popular vehicle to maximize excess cash, money market mutual funds and sweep accounts maintain value while providing a higher yield than the average bank account. They offer a safe place to hold funds that are still easily accessible. While the Fed does not directly control money market yields, the yields typically track closely to the Fed Funds Rate. That said, money market yields are variable and susceptible to changes when the Fed makes changes. Money market vehicles pay interest monthly, a steady cash flow many investors prefer. Yields are currently above 5% for the two custodians with whom we partner (Fidelity and Schwab).

2. Certificates of Deposit (CDs)

CDs feature FDIC insurance for up to $250,000 per individual or entity per issuer. CDs are considered a risk-free investment up to the FDIC insurance level. TFG can shop the open market of CD issuers for the best rates at various maturities to meet a client’s need, and we are not captive to a single bank. CDs may pay interest at maturity, semi-annually, or monthly, depending on the issuer. The main drawback of CDs versus money market is liquidity. While money market vehicles hold their value constant, like a bank account, CD values can vary. If the need arises to sell early, you may have to sell at a discount on what you paid. CDs currently yield over 5% for up to 5 years.

3. U.S. Treasury Bonds

U.S. Treasury bonds are one of the safest options for investors with excess cash. Treasury Bills, or T-bills, mature in 12 months or less, pay no interest, but are sold at a discount to the amount you receive at maturity. Treasury Notes mature later than 12 months and pay semi-annual interest. Being backed by the full faith of the United States government, coupled with the US Dollar being the global reserve currency, these instruments are considered risk-free from a default perspective. The Treasury market is among the most liquid markets in the world, so it is easy to sell a Treasury back to the market before maturity if a liquidity need arises. Treasury yields are currently 5% or better for up to 2 years.

4. Municipal Bonds

For investors in a high-income tax bracket, municipal bonds may be the best solution for excess cash. Most municipal bonds are issued with tax-exempt interest payments, meaning interest paid by the bonds is not federally taxable, and many bonds are also state tax-exempt, depending on your tax residence. A variety of municipal bond types are available. The main two options include general obligation bonds backed by the power to levy taxes and revenue bonds that rely on specific projects, like toll road construction or utilities, for repayment. Yields vary widely by state, municipality, and type of bond. For example, Georgia State General Obligation bonds currently yield around 3.2% up to 5 years, equating to a 6.0% pre-tax yield for Georgia residents in the top income tax bracket.

5. Corporate Bonds

Corporate bonds are debt securities companies issue to raise capital for specific purposes, such as expansion, debt refinancing, or working capital. Like government-backed bonds, they offer investors periodic interest payments during the term and a total return of principal upon maturity. Corporate bonds vary in credit quality, from investment-grade bonds issued by financially stable companies to riskier high-yield bonds from companies with lower creditworthiness. The trade-off with corporate bonds is they offer higher yields than government bonds but with increased default risk. This risk can be mitigated by investing in bonds issued by the most credit-worthy companies. AA-rated corporate bonds currently yield 5% or higher for up to 5 years.

A Timely Strategy

It’s important to note that there isn’t a “one-size-fits-all” solution for optimizing yield on excess cash.

What to invest in depends on a mosaic of factors, including:

- amount being invested

- upcoming specific needs for the money

- yield competitiveness among the above types of money market and bonds

- shape of the yield curve

For example, an investor might have cash from a recent real estate transaction and want to invest it conservatively. The Fiduciary Group can create a bond ladder, a customized bond portfolio with different maturity dates, to manage interest rate risk and maintain a steady income stream. Each bond in the ladder matures at a different time, allowing the investor to reinvest the principal from maturing bonds into new bonds at current market interest rates. This strategy balances growth and income with the flexibility to capture higher interest rates when they become available. This strategy also keeps your wealth from being concentrated in a single category or timeline. It is all catered to the unique circumstances of individual clients.

As always, investors are invited to contact us for more information regarding Fed activity, interest rates, and low-risk options for investing cash. We can help evaluate if there is excess cash in the context of your financial plan and recommend ideas to generate higher yields on savings.