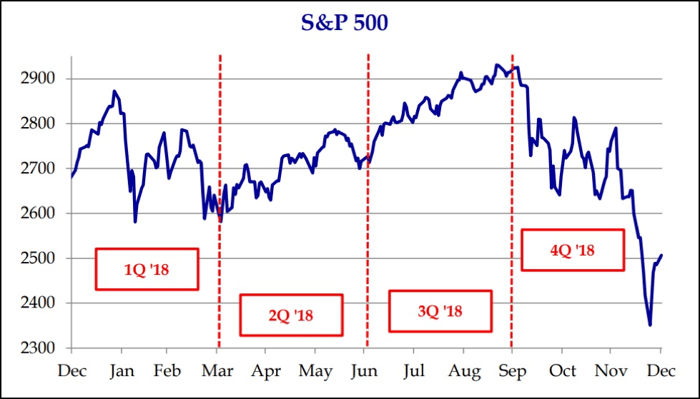

Through the first nine months of the year, it looked like 2018 would be another pleasant year for investors. The S&P 500 climbed more than 7% in the third quarter, pushing the year to date return for the index above 10%. But those gains – and then some – evaporated in the fourth quarter, with the S&P 500 falling roughly 20% (peak to trough) from its highs in late September. For 2018, the total return for the S&P 500 was a loss of 4.4%.

As usually happens when the waters turn choppy, the financial media has paraded out an endless list of commentators who are happy to explain how we got here and to guess where we’re headed next. The possible explanations for our current pain range from tariffs and a slowdown in global economic growth to algorithmic / high-frequency trading and “higher uncertainty” (by definition, we would think the level of uncertainty at any point in time is always, well, uncertain). Whatever the reason(s), the question people really want answered isn’t how we got here – it’s where we’re headed next (and more specifically, whether stock prices will go up or down as a result).

We don’t know the answer to that question. The reason why is because we do not profess any ability to predict short-term market movements. We also think it’s difficult, if not impossible, to consistently make predictions about future macroeconomic and political developments that are both contrarian and accurate (commonly held beliefs are already accounted for in market prices). The evidence suggests others, including the self-proclaimed experts, are in the same boat as us.

Our solution is to take a different approach. In our client communications we’ve consistently stressed the importance of maintaining a long-term perspective. As opposed to trying to get ahead of short-term moves in either direction, we are focused on constructing portfolios such that our clients can comfortably maintain their asset allocations throughout the market cycle. Said differently, we accept the fact that we cannot predict bouts of volatility. Instead, we focus our attention on preparing client portfolios (and clients themselves) for its inevitable occurrence.

The other message we’ve repeated is the importance of asset allocation and diversification. We do this to ensure our client’s portfolios are aligned with their future cash needs (their ability to bear risk), as well as their capacity to handle the sweeping emotions that come with material changes in their accounts value (their willingness to bear risk). We need to ensure that both of these conditions are met when the pressure is most intense (at the bottom of the cycle). A sound long-term plan isn’t worth the paper it’s printed on if it can’t be sustained during tough times.

The past couple of months have been unkind to equity investors. Clients are opening their account statements to portfolio values that are materially lower than they were ninety days ago (if it’s any solace, we’re invested alongside our clients and are feeling the pain as well).

At these times, investors are prone to emotional responses – “Look how much my portfolio has gone down! Should I sell now and worry about getting back in once the uncertainty passes?”

That quickly deteriorates into a guessing game (market timing by another name). We’ve seen others try their luck at this in the past, including at every point of unease during the current market cycle. They’re almost always worse off for doing so. Selling may provide comfort in the moment, but it fails to consider the most important question as it relates to a long-term strategy: “what next?” Our goal is to own high-quality businesses that generate value for their owners over time. The best way to do that is to find said businesses and stick with them through thick and thin. As noted earlier, we do not believe that trying to dance in and out of equities (while paying trading costs and capital gains taxes along the way) is an intelligent long-term strategy.

This isn’t the first time we’ve been here, even in the current bull market (granted, this pullback has been deeper and more sudden than the ones that preceded it). Most recently, investors voiced similar concerns during the correction in early 2016. The same truth that applied then holds now: abandoning a sound long-term plan to act based on short-term emotions is a mistake. This is the time to remind yourself that a long-term plan only works if you stick with it for the long run. It’s also the time to remember that lower prices sow the seeds for higher forward rates of return.

As always, the macroeconomic picture has its fair share of strengths and weaknesses. Broadly speaking, the U.S. economy is in good shape, but recent data points have been mixed. The unemployment rate is near a 50-year low, which supports the largest component of U.S. GDP – consumer spending. Recent U.S. holiday shopping results have been robust; however, consumer and business confidence measures have retreated from their record highs. Outside of the U.S., both China and Europe have softened, raising concerns about global growth. Trade tensions between the U.S. and China and the role of the Fed in 2019 are front and center, and positive news on either of these fronts would be welcomed by the market.

From a fundamental perspective, we believe that equity valuations appear attractive at current levels – particularly relative to current interest rates and the paltry returns offered by high-quality long-term bonds. Following a significant increase in S&P 500 profitability in 2018, as well as lower stock prices, we’ve seen a meaningful contraction in the market multiple over the past year. With that said, it’s always worth remembering that reasonably priced (or even cheap) stocks can get cheaper in the short-term.

We continue to believe that a balanced approach is prudent. We’re encouraged that recent market turmoil presents us with the opportunity to invest in some high-quality businesses trading at attractive valuations. In addition, fixed income portfolios are doing their part by generating income and providing some diversification benefits (downside protection) during the correction.

As we look ahead to 2019, we continue to believe that our clients are best served by holding globally diversified portfolios with an asset allocation that accounts for their unique needs. As always, please feel free to reach out if you have any questions.