At The Fiduciary Group, we serve as fiduciary investment advisors. This means that we are required to act in the best interest of clients and to not place our own interests ahead of clients. As part of this relationship, we have the discretion to act on our client’s behalf and we endeavor to make thoughtful and rational investment decisions. In this note we’ll discuss the value we strive to provide as part of a discretionary investment management relationship.

Financial Objectives

We begin by seeking to understand our client’s long-term financial objectives. We then balance the client’s financial objectives with their willingness and ability to bear risk. We prepare an investment policy statement (IPS), which is a guiding document that provides a framework for how we will manage the portfolio. Our approach to portfolio construction may vary depending upon the client’s unique circumstances.

Portfolio Construction

As we outlined in a recent note, we believe asset allocation should be more structural than tactical. Said differently, we believe investors should focus on finding an appropriate allocation and sticking with it. Our goal is to construct a portfolio that will enable our clients to remain level-headed throughout market cycles and avoid the bouts of euphoria and despair that encourage the reactionary decision-making that can negatively impact portfolio returns. We believe that identifying and building a portfolio with an appropriate asset allocation for the long run is critical to withstanding market volatility.

We try to be thoughtful in every decision we make. We analyze potential investments on their own merits, but we also spend time thinking about what an asset may contribute in the context of a broader portfolio. By design, it’s unlikely we will have a portfolio where every asset is simultaneously generating strong returns (the inverse should be true as well). We operate under the belief that trying to predict short-term market movements is a fool’s errand. For this reason, we maintain exposures to various asset classes and geographies with the purpose of constructing a portfolio that provides an experience that accounts for each client’s risk tolerance, cash needs, and long-term financial objectives. Naturally, we remain flexible as our client’s circumstances change.

The Behavior Gap

Our most pronounced opportunity to add value typically shows up during periods of market volatility. It’s during these challenging market environments that a sound, long-term plan can be disrupted by impulsive or emotional decision-making. Notable examples include piling into the market after a strong move to the upside (near the highs) or capitulating and selling when the pain becomes too much to handle (near the lows). Unsurprisingly, the end result when you buy near the highs and sell near the lows is discouraging.

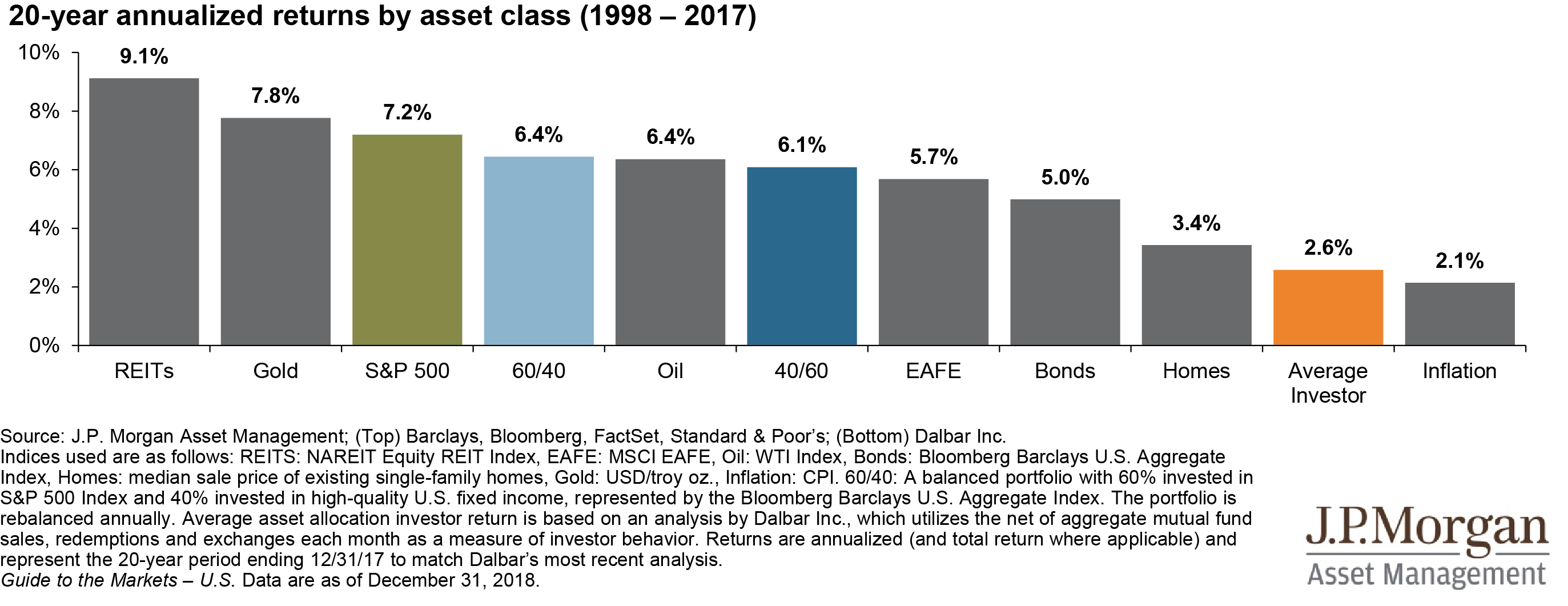

The data supports this conclusion. As you can see in the chart below, the “Average Investor” has only returned 2.6% annualized over the past 20 years, underperforming nearly every major asset class. Over the same period, a portfolio with 40% invested in stocks and 60% invested in bonds has returned 6.1% per year. On an initial investment of $1 million, that’s the difference between ending with $1.67 million and $3.27 million after two decades. Clearly the cost of this emotional decision-making has been significant for the “Average Investor.” We suspect this is largely due to investors attempting to predict market swings or shortening their time horizon during periods of market volatility. Again, we address this potential pothole by taking the asset allocation decision off the table (by maintaining a structural allocation). Experience tells us that large shifts away from a set strategic allocation can be one of the most harmful actions an investor can take.

Other Common Pitfalls

One of the biggest hurdles that discretionary managers face is client directed trades. The client often assumes that the directed purchase isn’t a big concern because it will only be a small percentage of the portfolio. But this practice, known as “narrow framing” (a tendency to make investment decisions without considering the context of the total portfolio), can have a significant impact on the management of the portfolio. It’s important to understand that this has nothing to do with whether the client directed trade is a “good or bad” idea on its own merit. Instead, it has to do with the impact of that decision in the context of a broader investment strategy (portfolio).

Nibbling at the portfolio to fund purchases counter to the strategy may result in an incoherent portfolio. Every trade that moves us away from the strategy we’re trying to implement has the potential to become problematic. Directed purchases can lead us to misallocations among various asset classes or industries and therefore leave us exposed to unwanted or underappreciated risks.

Some recent examples of client directed trade requests include bitcoin, marijuana stocks, and tech IPO’s. Usually these requests, especially during a long running bull market, are triggered by the fear of missing out (or “FOMO”) on the next big thing. This is a potent emotion that we deal with ourselves. But history has consistently shown us that chasing what’s hot at the moment can be a disastrous investment strategy. For that reason, we try and encourage our clients to maintain a focus on the long-term as opposed to jumping between the investment trend of the day.

At the other end of the spectrum, clients tend to have a keen focus on any losses on their portfolio statement. It can be difficult for a client to understand why we have not sold an asset that has performed poorly. Many advisors deal with this problem by dumping anything that has done poorly, even if they don’t think that’s the best investment decision for the long run (simply put, this can be a much easier route than being forced to discuss the investment ad nauseum).

While that may be the easier route, we don’t think it’s the right one. When assessing an underperforming asset, our focus is on whether the prospects of the company or investment have changed. If the answer is yes, we will sell. But many times, underperformance can be a function of an asset class or industry being out of favor. That is something we expect to happen and are comfortable dealing with. This is the reason why we hold broadly diversified portfolios that are not over exposed to any individual security, geography, or asset class. Again, the important thing to do is to think about the investment in the context of a broader portfolio, not to narrowly focus on the short-term changes in the market price of a single holding.

Conclusion

The overarching purpose of what we do as fiduciary investment advisors is to promote rational decision-making and to help clients maintain their focus on their long-term financial objectives.

Success in investing doesn’t require an off the charts IQ. Instead, it demands the temperament to stay committed to a long-term plan and the ability to avoid common behavioral mistakes.