Funding a child’s or grandchild’s education is a high-priority savings goal for many families. This article will answer a few important questions:

1. How much will college cost?

2. How much do I need to save to fund the estimated expenses?

3. What types of accounts should I use to save for and pay for college?

4. How should I invest the savings?

This article focuses on self-funding the cost of college. Other funding sources such as loans, grants, and scholarships, as well as tax credits for education expenses, are re- sources that families should explore, but they are beyond the scope of this article.

How much will college cost?

A good starting point to find out the current cost of colleges and how fast those costs are going up is col- legecost.ed.gov, a site designed and maintained by the U.S. Department of Education. It allows users to compare colleges’ tuitions and fees, net price, and other characteristics. Once you know the actual cost of the college(s) under consideration and the average inflation rate for that college’s tuition and fees, you can plug that information in to any number of college cost calculators available on the web. One such calculator can be found on bigfuture.collegeboard.org. If you don’t have exact costs, you can use the average cost provided by The College Board for different types of colleges.

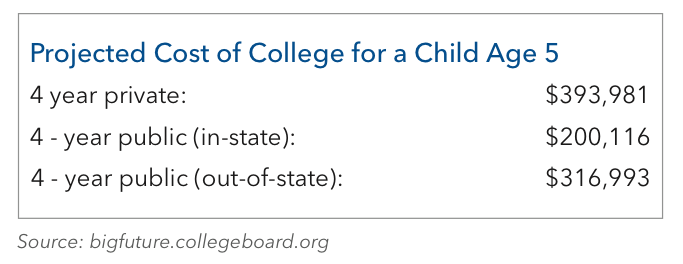

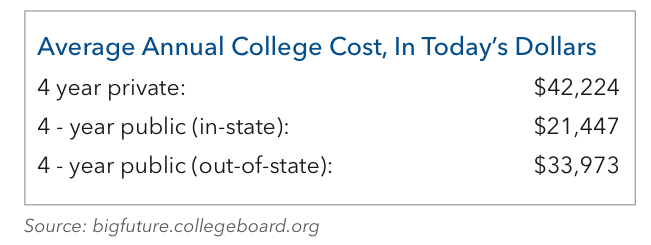

The college cost calculator estimates the cost of college by the time a child enrolls. The factors which come into play are the annual college cost in today’s dollars, the college tuition inflation rate (how much it goes up every year), the expected number of years of attendance, and the years until college. Here is an example of the output, applying the national average tuition inflation rate of 6%, an expected attendance of 4 years, and an assumption that the child is 5, thus 13 years away from enrolling. Assuming a continuation of the national average tuition rate, in 13 years the average private college tuition will have risen from $42,224 to $90,061, the average public (in-state tuition) will have risen from $21,447 to $45,745, and the average public (out-of-state) tuition will have risen to $72,462, up from $33,973.

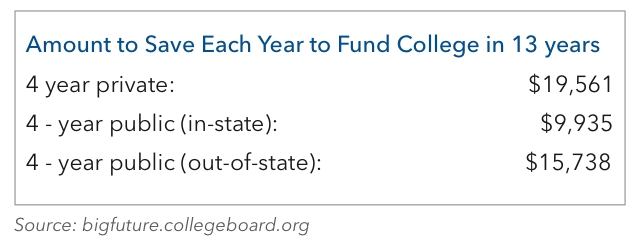

So the next question in our example is: how much do the parents of a 5-year old need to save every year to have funded the child’s college education by the time the child is ready to go to college?

How much do I have to save each year?

If you are mathematically inclined, you can calculate the amount you must save each year to reach your total savings goals using a financial calculator (otherwise you can ask your investment advisor to make the calculation for you). In our example, N = 13 (how many years to save), i = 7 (assume annualized returns on the investments of 7%), FV = $393,981, $200,116, or $316,993 (the projected future cost, depending on which type of college), and PV = $0 (no savings thus far). The chart below solves for PMT (the required amount to save each year to reach the savings goal):

What types of accounts should I use to save for educational expenses?

Parents can of course save to their own (taxable) investment account(s) for their children’s education. There are several other types of accounts for funding educational expenses which offer some tax advantages:

Section 529 Plans: Most states sponsor a 529 plan, and in many states, you do not need to be a resident to participate (though non-residents do not benefit from any state tax deductions offered). Anyone can contribute to a 529 plan for a child (parents, grandparents, uncle/ aunt, friend).

The most popular variety of 529 plans is a qualified tuition plan. This is a tax-deferred investment account utilizing mutual funds (investment options differ from state to state). In 2015, up to $14,000 ($28,000 for married couples) per beneficiary qualifies for an exclusion from the federal gift tax. If the contribution exceeds this limit, the account owner may elect to treat up to $70,000 ($140,000 for a married couple) as having been made over a period of up to five years. Total contribution limits vary by state, ranging from $235,000 to $452,210.

Not only do the investments grow on a tax-deferred basis, but the money can be taken out on a tax-free basis if used to pay for qualified education expenses. Qualified expenses include tuition, room and board, travel, necessary equipment, and other costs. In addition, some states, including Georgia, allow contributions by residents to be deductible at the state level (Georgia allows a deduction of $2,000 per beneficiary on state income tax). Unused amounts may be rolled over to a 529 plan for another beneficiary from the same family without penalty.

Coverdell Education Savings Accounts (ESA): ESAs allow for non-deductible contributions up to $2,000 per year for each child up to the age of 18. Earnings on funds in the ESA are tax-deferred and distributions are tax-free provided they are used for qualified education expenses. Unlike a 529 plan, which may only be used for college, ESA distributions may also be used to pay for K-12 elementary education. However, the amount that can be contributed is reduced when a married couple’s AGI reaches $190,000, and is eliminated when the joint filers’ income reaches $220,000. ESAs must either be rolled over or distributed by the time the child reaches 30 years of age.

UGMA and UTMA: Anyone may also set up a custodial account for a minor child under either the Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA). There is no contribution limit to these accounts, and the funds may be used to pay for any expense for the benefit of the minor (not just qualified education expenses). Contributions are not tax-deductible, and earnings on the account are taxed to the minor. For those under 19 (age 24 if a student), in 2015 the first $1,050 of earnings is tax-exempt, the next $1,050 is taxable at the minor’s rate, and any remaining income is taxed at the parents’ rate. After age 19 (24 if a student), all income over $1,050 is taxed at the child’s rate. At the age of majority, the assets are completely in the control of the child.

How should I invest the savings?

The investment options available in Section 529 plans are determined by the state sponsoring the plan. Most of these plans offer a variety of risk-based balanced mutu- al funds as well as asset allocation funds based on the child’s age (the glide-path allocation funds become more conservative as the child approaches college age). You can choose the appropriate investment at the time you set up the plan, as well as up to twice annually thereafter. Investment decisions for an ESA account are made entirely by the trustee (as directed by the donor), and the options are fairly broad as long as they don’t violate the allowed investments for an IRA. Investment decisions for an UGMA or UTMA account are made by the custodian until the minor reaches the age of majority, and relatively few investment restrictions apply. There are three important keys to balance in choosing an investment strategy: time horizon, return objectives, and risk tolerance. The longer the time horizon until the funds are needed, the more risk you can afford to take. Stocks historically have returned 8-9% with high volatility, and bonds have returned 4-5% with low volatility. The balance you choose between stocks and bonds will de- termine both the rate of return as well as the volatility of your investment portfolio. If you start saving to a college fund when the child is 3-5 years old, your time horizon is 13-15 years. Pursuing an aggressive strategy in the early years and gradually moderating your exposure to stocks as college age approaches should allow you to achieve an annualized return over that period of about 7% while appropriately managing risk. Bottom line for all those saving for a child’s education: start early; plan realistically; save to the plan; and invest appropriately.