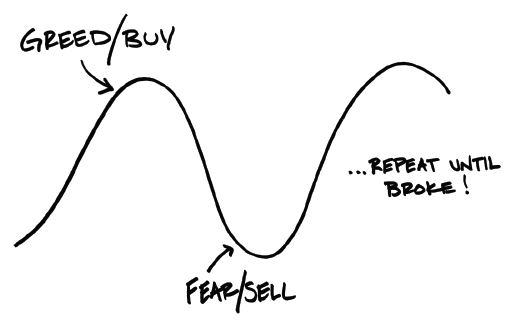

Emotions can cause investors to do the wrong thing at the wrong time. We all know, rationally, we should buy low and sell high. Yet emotions can cause investors to do just the opposite.

Market cycles—and the emotions that they incite—can feel like a roller coaster ride.

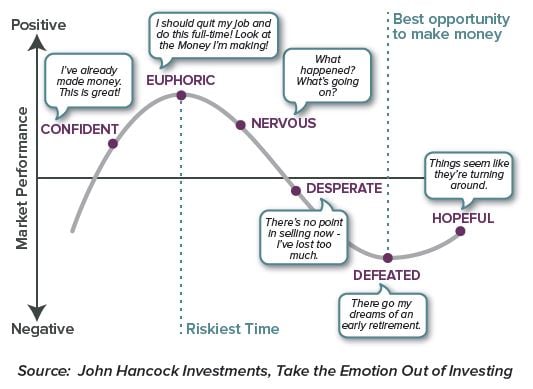

When the stock market is rising, investors feel confident and want to pile in. As prices reach all-time highs, euphoria sets in, leading investors to feel that prices will just continue to rise. However, what goes up will inevitably go down. As prices fall, investors become nervous and fearful. The low point of a market cycle is often the best time to make money, but only if the investor stays invested. Unfortunately, the emotions of desperation and defeat often drive investors to “get out” at market lows, thereby locking in losses. As the markets rebound, investors become hopeful and may begin to invest again, but at higher price levels than those at which they sold. Some investors feel regret, taking an “I’ll wait till the markets come back down” approach, and sit on the side lines during rising markets.

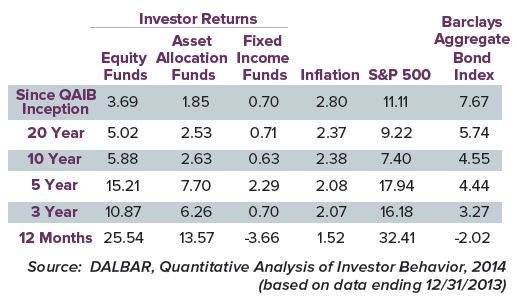

Riding the emotional rollercoaster can lead to self-defeating behavior. Each year the independent research firm DALBAR publishes the returns of the “average” mutual fund investor versus the indices. The disparity in returns, particularly over the long-term, is significant. Over the last 20 years, the annualized return for the average equity fund investor was only 5.02% compared to the S&P index average annual return of 9.22%.

DALBAR’s research showed that the results were more dependent on investor behavior than on fund performance. Mutual fund investors who hold on to their investments are more successful than those who try to time the market. DALBAR reported that the greatest losses occur after a market decline. Investors tend to sell after experiencing a “paper loss” (a drop in the valuation of their portfolio in their quarterly statement)— the classic “sell low” behavior—and start investing only after the markets have recovered their value— the classic “buy high” behavior. The harmful result is participation in the downside while being out of the market during the rise. This is what leads to a discrepancy between “investment returns” and “investor returns.”

Emotions are not rational, so it’s hard to counter them with logic. However, there are three actions we can take to better manage our response to emotions so that they don’t jeopardize our investment success: embrace volatility; make a plan and stick to it; and stay focused on the long-term.

Embrace Volatility

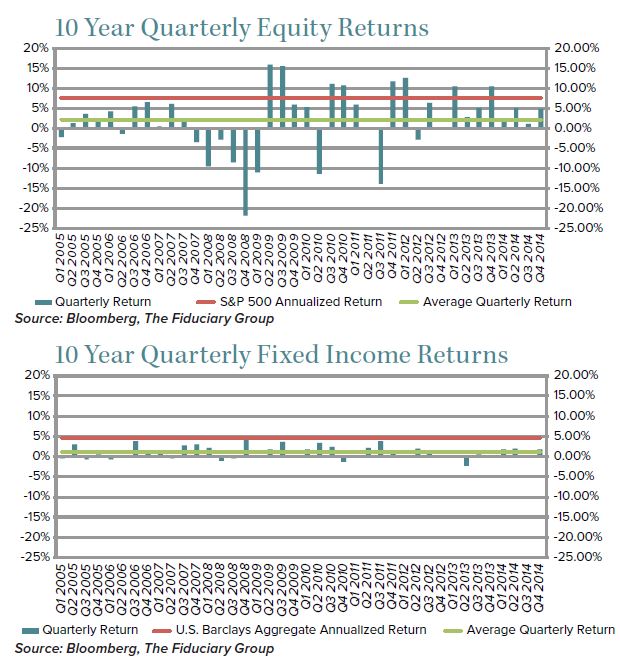

We tend to think of volatility as a bad thing. But volatility has two sides. Volatility to the upside is welcome. It’s really only downside volatility that gets us upset. Volatility— seen as our friend rather than foe—offers opportunity as well as risk. When markets are down, prices are cheap and it’s a good time to buy. When markets are up, it’s a good opportunity to sell and take some profits. Let’s take a look at the volatility in short-term returns over the last 10 years in the major stock and bond indices. The charts below plot the quarterly returns of the S&P 500 and the Barclay’s Aggregate Bond index from 2005 through the end of 2014. The red horizontal line running through each graph is the 10-year annualized return for that time period. The green horizontal line is the average quarterly return for that time period.

Over the last 10 years stocks were significantly more volatile than bonds, meaning the returns from period to period had larger swings, the highs were higher, and the lows were lower. However, stocks had a higher annualized (average annual compounded) return for that time period: 7.67% for stocks compared to 4.71% for bonds.

The picture from the last 10 years is not radically different from historical norms. Historically, the S&P 500 has returned long-term a nominal annualized return of about 9% with high volatility. Bonds have had a long-term nominal annualized return of about 5% with relatively low volatility.

Embrace volatility as a normal and natural part of investing. Get your arms around the fact that the portion of your portfolio that is invested in stocks will return very erratic returns over shorter time periods—sometimes high and sometimes low—but in the long run those investments should lead to average annualized returns of 8-9%. The portion that is in bonds will be much less volatile, and over the long term should return between 4-5% on an annualized basis. If you really know what to expect, and embrace it—getting neither euphoric when prices are up or defeated when prices are down—you’ll be better able to ride it out.

Have a Plan

Having a strategic plan is the starting point for managing risk and avoiding impulsive behavior. The key pillars of an investment plan are diversification, asset allocation, and rebalancing.

Asset allocation means deciding how much of your portfolio to invest in the different asset classes: stocks, bonds, and cash. Determining the right asset allocation involves thinking about the goals you have for the different portions of your investment account, the time horizon for those goals, and the risk you can afford to take in valuation swings relative to those goals. For example, is a portion of the money in your investment account to be used in the near term to buy a home or pay for a child’s education? Is the account to provide income for life in retirement? Maybe the goal is to leave a legacy for children or charities?

The portion of your account that is for longer-term goals (10 years+) should be allocated primarily to stocks because growth is the priority and short-term volatility does not pose as much of a risk. The portion of your account intended for goals which are to be realized in the mediumterm (the next 5-10 years) may favor stocks but incorporate some bonds to moderate volatility. Assets intended to satisfy goals that are to be reached in the next 2-5 years may be weighted more to bonds to moderate volatility, but with some portion of stocks for growth. Finally, the portion of the portfolio intended for use in the next 2 years should be short-term fixed income and cash equivalents, as preservation of capital is key.

Diversification refers to how you divide up your investments among and between investments within each of those broad classes. For example, within the portion being allocated to stocks, you want to divide the investments appropriately between different geographies (domestic, international, emerging), market capitalization (large, mid, and small cap), and strategies (growth, value, blend). The chart below shows how diversification can smooth out the volatility in returns of the different individual asset classes. The diversified portfolio used in the example below is a balanced growth strategy (70% stocks and 30% bonds).

Rebalancing is the best way to give yourself the highest likelihood of buying low and selling high in a systematic, unemotional way. Rebalancing means returning your portfolio to its original target allocations. For example, if your target allocation is 70% in stocks and 30% in bonds, following a downturn in the stock market the actual portion that stocks comprise of your portfolio might have slipped to 60 or 65%. When you rebalance, you sell bonds (whose price went up relative to stocks) and buy stocks (whose price is down) so that your portfolio again returns to a 70/30 split. Rebalancing can be done on a calendar basis (for example, at the end of every quarter), and/or when the portfolio allocations stray more than a designated percentage from their target.

Stay Focused on the Long Term

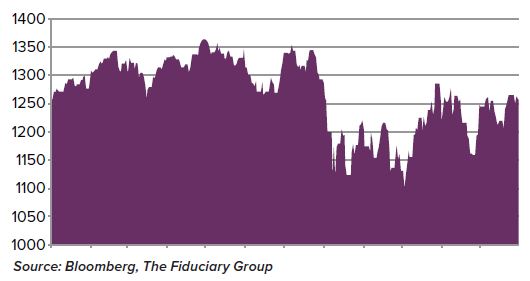

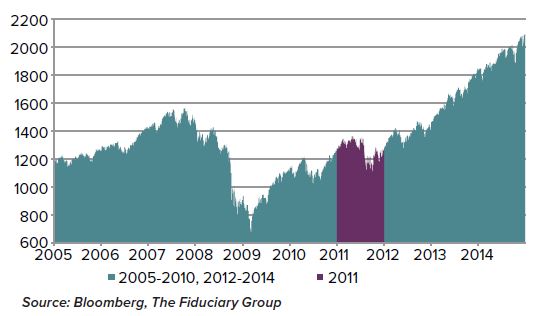

Expanding our view from short term returns and short-term volatility to the longer term results gives us an entirely different outlook on our portfolio and the risk/return reward. Take a look at the following returns of an investment in the S&P 500. If you viewed only the volatility you endured during the period of that investment and the fact that at the end, you weren’t any better off (in fact, slightly behind where you started), you would not feel very good about that investment and probably want to get out of it.

The returns pictured in the purple graph were actually the S&P returns from the year 2011. Now, just expand your view to the 10-year period from 2005 through 2014. The impact of being invested in 2011 is completely different when seen within the outcome of staying invested over a longer time frame. During the years 2005-2014, you would have experienced a lot of volatility (including the financial crisis in 2008). But now, viewed in the context of a full investment cycle of 10 years, the volatility would seem worth it. In that 10-year time period your portfolio would have returned an average annual return of about 7.7%.

In conclusion, the best way to put the brakes on the emotional roller coaster is by practicing the following:

• Accept that short term volatility is a normal and natural part of investing. Embrace it and seek to exploit the opportunities it provides;

• Make and stick to a sound investment plan, which means investing in an appropriately allocated, globally diversified portfolio that is systematically rebalanced to your targets; and

• Ignore the noise and short-term market swings. Stay focused on the long-term results and whether those results are reasonable risk-adjusted returns in line with the goals for which those funds are intended.